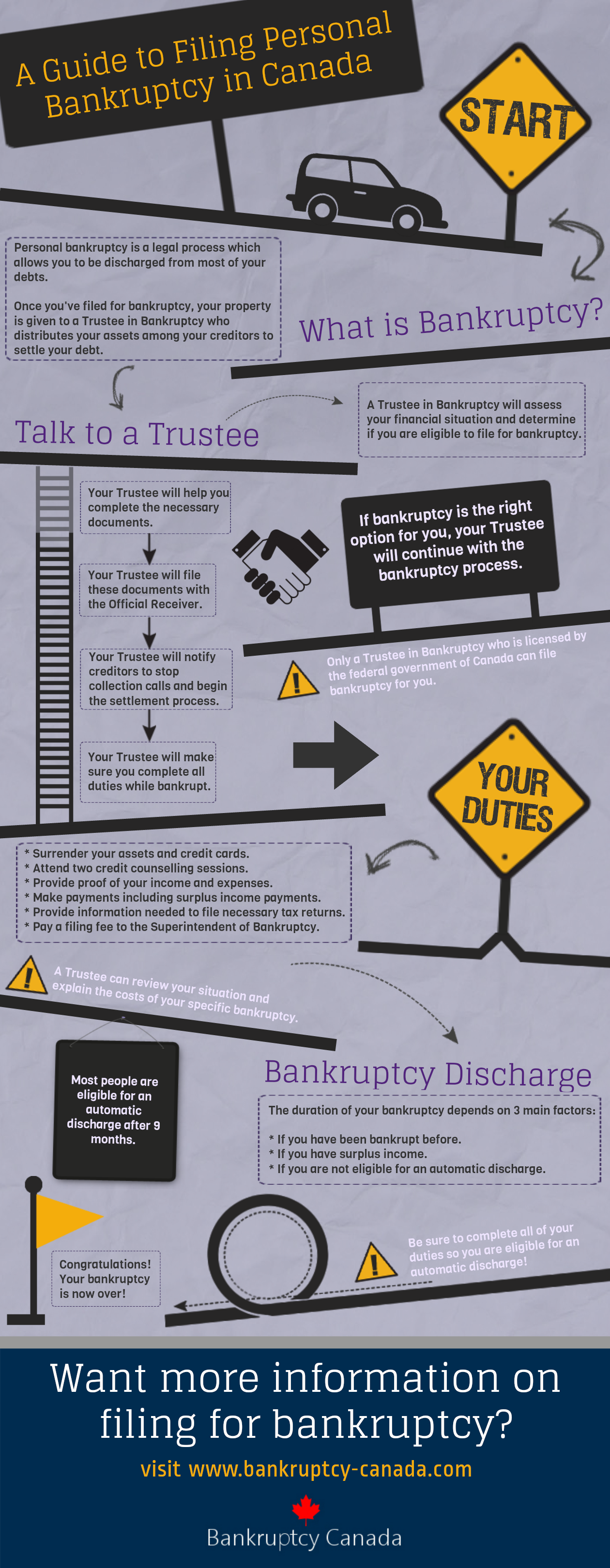

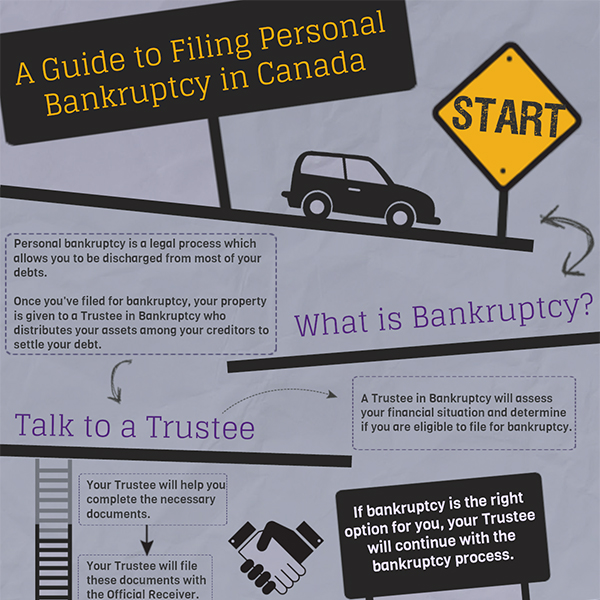

Okay, so you're thinking about hitting the reset button on your finances in Ontario? Let's talk about how to file for personal bankruptcy! Think of it as hitting the big red "emergency clean-up" button on your financial life.

First things first, you need to find a licensed Bankruptcy Trustee. These are the official referees in the bankruptcy game.

Finding one is like searching for the perfect avocado – you want one that's just right! You can find a list on the Government of Canada's website.

Step 1: Chat with a Trustee

This initial meeting is usually free, so don't worry about breaking the bank before you even start! It's like a "get to know you" session for your finances.

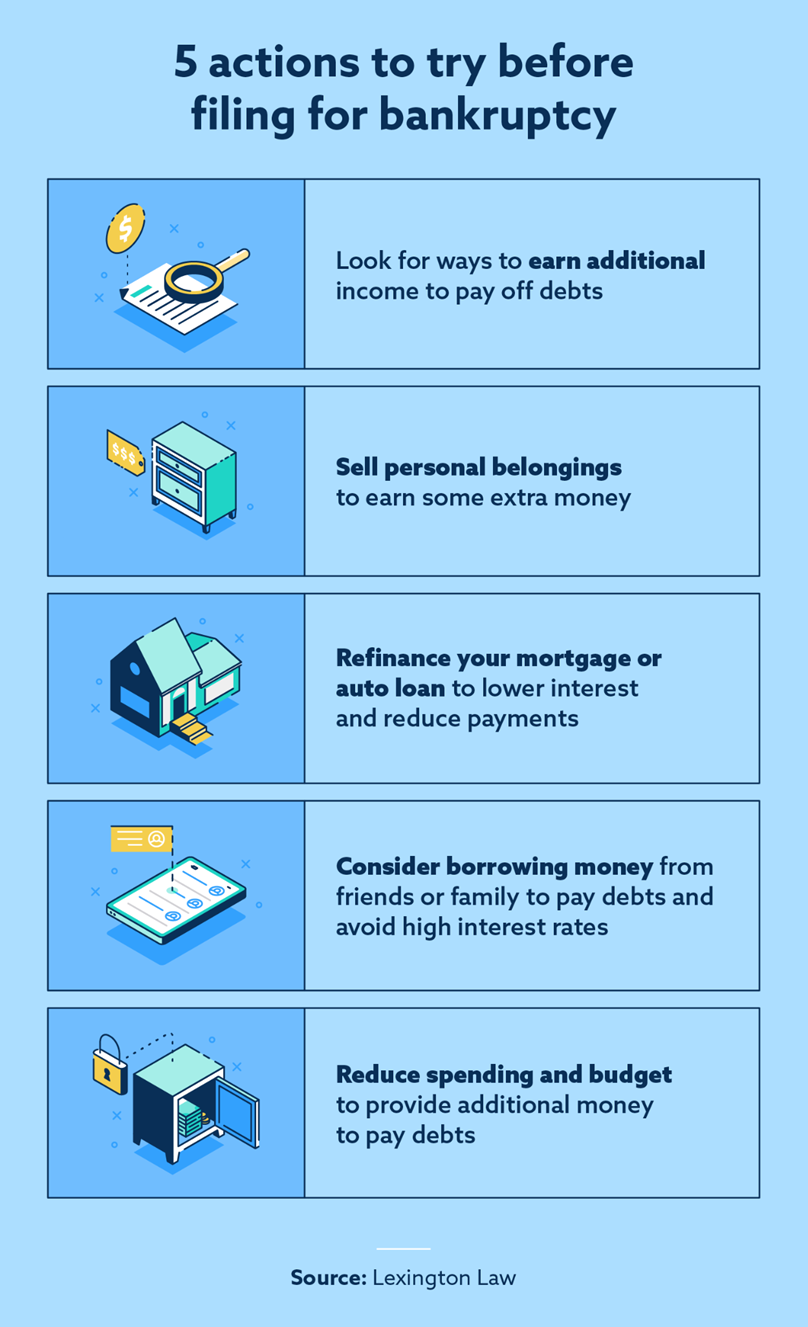

The Trustee will look at your income, debts, and assets. They'll also explain all your options, including alternatives to bankruptcy, such as a consumer proposal.

Imagine it's like going to a financial doctor – they diagnose the problem and suggest the best course of treatment.

Step 2: Paperwork Palooza!

Once you've decided bankruptcy is the right path, get ready for some paperwork. Don't panic; it's not as scary as it sounds!

You'll need to fill out forms detailing your financial situation – think of it as a financial autobiography, the unedited version. Be honest, be thorough, and remember that every "i" needs to be dotted and every "t" crossed.

The Trustee will help you with all the forms, so you won't be navigating this jungle alone.

Step 3: Filing the Paperwork

Your Trustee will file all that paperwork with the Office of the Superintendent of Bankruptcy. That's a mouthful, isn't it?

This is the official moment! You're now officially in bankruptcy. Don't worry, it's not like a flashing neon sign announces it to the world.

Consider it like sending a formal invitation to your creditors to, well, stop hounding you directly!

Step 4: Duties During Bankruptcy

During your bankruptcy (usually 9 or 21 months), you have a few responsibilities.

First, you need to attend two counseling sessions. These are designed to help you learn about money management and avoid future financial troubles. Think of it as financial boot camp, but without the push-ups!

You also need to report your income to the Trustee. Any surplus income (over a certain threshold) will go towards paying down your debts. Time to find some creative ways to budget!

Basically, cooperate with the Trustee, attend the counseling sessions, and be honest about your income. Simple, right?

Step 5: Discharge and Fresh Start

Once you've completed all your duties, you'll be discharged from bankruptcy. Cue the confetti!

This means your debts are legally wiped away. You get a fresh start, a clean slate, a financial do-over! You are free from the burden of those old debts.

It's like graduating from financial hardship school. You did it!

Important Note: Bankruptcy isn't a magic wand. It can affect your credit rating, so be prepared to rebuild it.

However, with smart financial decisions and a bit of planning, you can get back on track in no time.

So, that's the basic rundown of filing for personal bankruptcy in Ontario. Remember to talk to a licensed Bankruptcy Trustee for personalized advice. Good luck!

Disclaimer: This is a simplified overview and not legal advice. Always consult with a qualified professional for specific guidance on your situation.